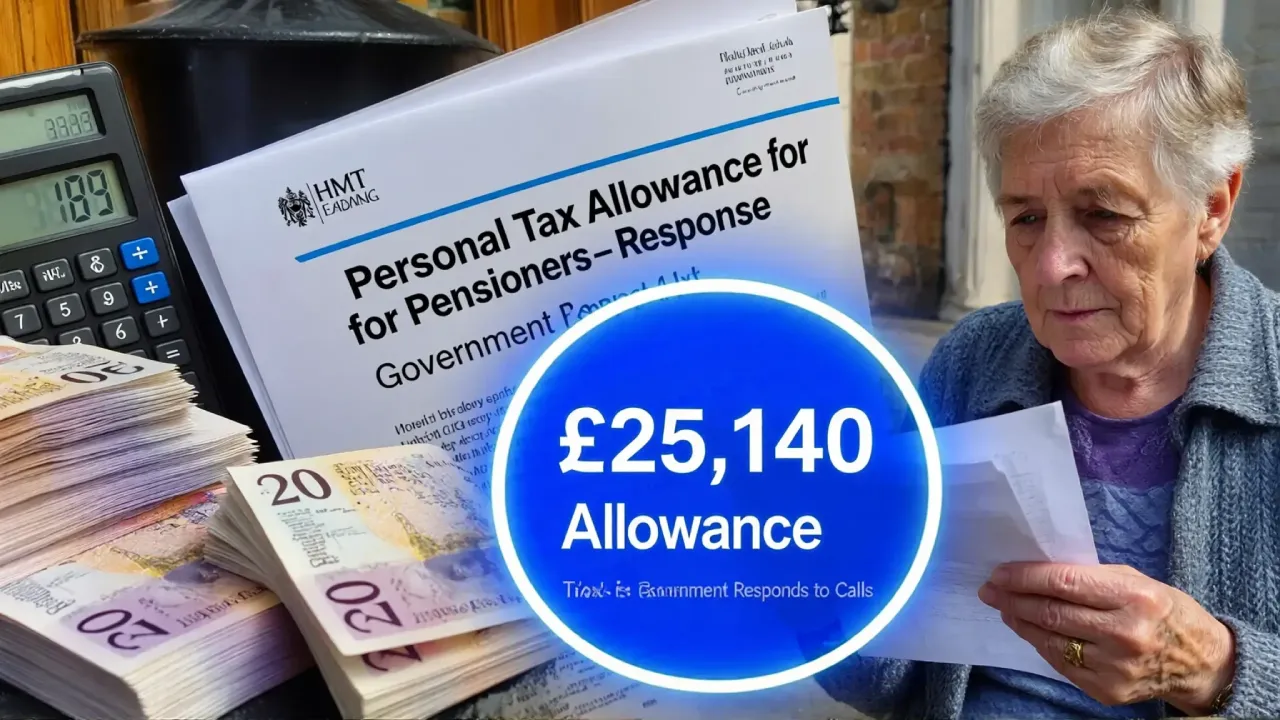

The debate over tax fairness for pensioners has returned to national attention after renewed calls for a higher personal tax allowance for older people. Campaigners, charities, and several MPs are urging the UK Government to raise the personal tax allowance for pensioners to £25,140 — a figure that matches the full annual value of the new State Pension.

This article explains what the £25,140 proposal means, how the government has reacted, and what pensioners should realistically expect in the months ahead.

Why the £25,140 Figure Matters to Pensioners

The £25,140 threshold is not an arbitrary number. It reflects the annual value of the full new State Pension following recent increases.

Campaigners argue that if the State Pension exists to provide a minimum standard of living, taxing it undermines its purpose. For many pensioners, income tax does not feel like a contribution from surplus earnings — it feels like money being taken away from essential household budgets.

Current Personal Allowance Rules Explained

The standard personal tax allowance in the UK currently stands at £12,570. Anyone earning above this level — including income from pensions — may have to pay income tax.

This allowance has been frozen for several years. During that time, both wages and pensions have increased, a process commonly referred to as fiscal drag. As a result, more people are paying tax even though their real incomes have barely changed.

For pensioners, this means:

- The State Pension alone can push income close to the tax threshold

- Even a small private pension can trigger tax liability

- Many retirees now pay tax for the first time after leaving work

Growing Pressure From Pensioner Campaign Groups

Pensioner advocacy groups have been increasingly vocal about the issue. Their core arguments include:

- Pensioners have already paid tax throughout their working lives

- State Pension increases are meant to protect living standards, not create tax bills

- Frozen thresholds disproportionately affect older people on fixed incomes

Campaigners believe aligning the personal allowance with the full State Pension would remove millions of pensioners from income tax altogether.

What the UK Government Has Said

In its official response, the government acknowledged the concerns raised by pensioners and MPs but stopped short of committing to any changes.

Ministers emphasized that the current personal allowance already offers significant protection from tax and highlighted other forms of support available to pensioners, including:

- Pensioner Cost of Living Payments

- Winter Fuel Payment

- Free bus travel and TV licences for eligible households

The government also stressed that increasing the allowance to £25,140 would come at a substantial cost to public finances.

Treasury Concerns Over the Cost

One of the biggest barriers to raising the allowance is the impact on tax revenue. Increasing the personal allowance for pensioners alone would reduce government income by tens of billions of pounds each year.

Treasury officials have warned that such a move could lead to:

- Higher government borrowing

- Spending cuts in other areas

- Higher taxes for working-age earners

These concerns have made ministers cautious, particularly during a period of ongoing economic uncertainty.

Why Many Pensioners Feel the System Is Unfair

Despite official explanations, many pensioners feel overlooked. A common frustration is that State Pension increases are widely publicized, only for part of the rise to be effectively clawed back through taxation.

For people living on fixed incomes, even modest tax bills can cause financial anxiety. Unlike working-age earners, pensioners often have limited options to increase income if costs rise.

The Impact of Frozen Tax Thresholds on Older People

The long-term freeze on the personal allowance has had a compounding effect. Each year the State Pension increases, more pensioners cross the £12,570 threshold.

This has resulted in:

- Unexpected first-time tax bills

- Confusing PAYE tax code changes

- Unplanned deductions from private pensions

In some cases, pensioners only discover they owe tax after receiving a letter, creating stress and uncertainty.

Political Reaction From MPs

Several MPs have publicly supported calls for reform, arguing that the tax system has not kept pace with demographic change.

Proposals put forward include:

- A higher personal allowance for pensioners only

- A partial or full tax exemption for State Pension income

- Automatic tax-free treatment of the State Pension

While none of these ideas have been adopted so far, political pressure continues to grow.

Is a £25,140 Allowance Likely in the Near Future?

At present, a full increase to £25,140 appears unlikely in the short term. The government has not indicated plans to introduce a separate allowance for pensioners.

Instead, ministers remain focused on targeted support payments rather than large-scale tax reform. However, future reviews of tax thresholds could reopen the debate.

What Pensioners Can Do Right Now

While policy changes remain uncertain, pensioners can still take practical steps to manage their tax position:

- Check tax codes regularly for accuracy

- Claim any available allowances or reliefs

- Use pension withdrawals carefully

- Seek free guidance from trusted charities or advisers

Even small adjustments can sometimes reduce or eliminate unexpected tax bills.

Why This Issue Is Unlikely to Disappear

With the UK’s ageing population and growing reliance on pension income, the tension between rising pensions and frozen tax thresholds is likely to continue.

Campaigners believe the issue will remain politically sensitive, particularly during election periods when older voters play a decisive role.

The Bigger Picture for Retirement Income

This debate raises broader questions about how retirement income should be taxed in modern Britain.

Many argue the system was designed for a time when pensions were smaller and private savings more generous. Today, millions rely almost entirely on the State Pension to meet basic living costs.

Hi, I’m Faiq, the person behind Asdbn. I started this website to share mobile and tech news in a simple and honest way. I regularly follow smartphone launches, updates, and trends, and I like to write about things that are actually useful for readers. My focus is to keep the content clear, genuine, and easy to understand, so anyone interested in mobile and technology news can benefit from it.